The EV standard Risk Profiler Questionnaire should be used only as a starting point for the discussion of risk. As with all questionnaires, there are a number of limitations which should be considered:

- Excludes investors who are not prepared to take any capital risk at all. Risk levels start at 'Little risk' not 'no risk'.

- It doesn't take into account capacity for risk. This should be discussed separately.

- Doesn't take into account other needs, objectives or circumstances

- Doesn't take into account the time horizon of any objectives, or the purpose of any investments for the purpose of assessing the attitude to risk, but an appropriate asset allocation for a given attitude to risk should take account of the time horizon.

- Target market averages may not be the same as the individual using it.

- Results will vary depending on where in the advice process the questionnaire is used. For example, if used before any fact finding at the start, it could be used by investors who are not prepared to do any investing because they have no capacity and / or are not willing to take any risk at all.

- Giving investors a guide to risk before answering the questionnaire could change the answers that are given. The questionnaire should be answered without intervention or help to get a truer picture, in the same way as giving a guide about behaviour and personality before answering a personality questionnaire would also affect the results.

- A client may say that they agree to the level of risk described, but do they actually know what impact this would have on them? Stochastic modelling can show this, including the benefits of diversification.

- Check that the model asset allocations and risk resulting from the questionnaire are still relevant to the individual investor given their objectives.

- The questions need to be considered as a whole. Inconsistent answers would require further discussion with the client to ensure they understand what they really want.

- It measures the attitude to risk at a point in time. As circumstances change the attitude to risk of an investor is also likely to change and should therefore be re-assessed.

- The intended target market is people who are looking to invest for a number of years. It has been assessed on investors being provided advice in the UK.

- The product and fund selection will affect the risk of the implemented strategy and should be reviewed to ensure it remains in line with the intended risk profile. For example, a fund with 'Cautious' in the name may not necessarily be appropriate for a 'Cautious' investor.

Yes. The questionnaire design has many rigorous steps which are outlined below. More details can be seen in our factsheet.

- Review the bank of questions available to ensure suitability for the expected user base

- Trial the questions with clients receiving advice

- Assess the questionnaire validity using statistical analysis

- Select the questions to ensure the range

- Allocate the scoring algorithm using independent expert groups

- Retest the questionnaire to ensure statistical robustness.

Chosen questions:

- Are clear

- Avoid complex language language

- Don't require prior investment knowledge

- Are not biased in the way they ask the question

- Are tested to be statistically proven to be representative of a client's risk

- Cover areas of emotional, scenario setting, past behaviour and self-assessment

The answer to each question is given a score, which when totalled is compared against a score card to identify the risk category. We also provide further detail on where within the risk profile banding the result lies.

The questionnaire is intended only as a starting point for discussion - it is important to document the reasons if the final risk profile is different from the calculated profile. In particular, the questionnaire is not designed to identify no-risk investors so this should be covered as part of the overall advice process.

Yes. Once the questionnaire is completed the opportunity to discuss and amend the risk category is given. If a change is made, a reason should be entered which will then appear on the report. This allows for checking of investor understanding and ensures full engagement throughout the process.

Risk levels are subjective and as a result there is no standard unit of measurement for investment risk. Instead, we use a scale which covers all investors taking some degree of risk against which the investor's attitude is compared based on the answers given.

The questionnaire will be suitable for a large proportion of clients. It is intended for those who wish to invest and is not suitable for clients who have no requirement or ability to take any investment risk on their portfolio. The trials for the standard questionnaire have been based on UK investment clients being provided advice. It can also be used in similar territories with a caveat that the client base has not been robustly tested.

An individual's attitude to risk is not considered to be dependent on the age of an investor. Clearly when the product and investment choices are considered age will be one of the additional factors which should be included.

The result of the questionnaire measures the attitude to risk of the investor at that particular point in time. Attitudes can change over time due to many factors, from the wider economic outlook to individual experiences. Therefore the assessment should be reviewed as required to ensure the risk profile is current during any subsequent advice.

The EV questionnaire now comes with an additional graphic which shows where within the risk category the investor's risk profile is situated. This allows discussions around suitability of various investments and will help to ensure the investment selected remains appropriate.

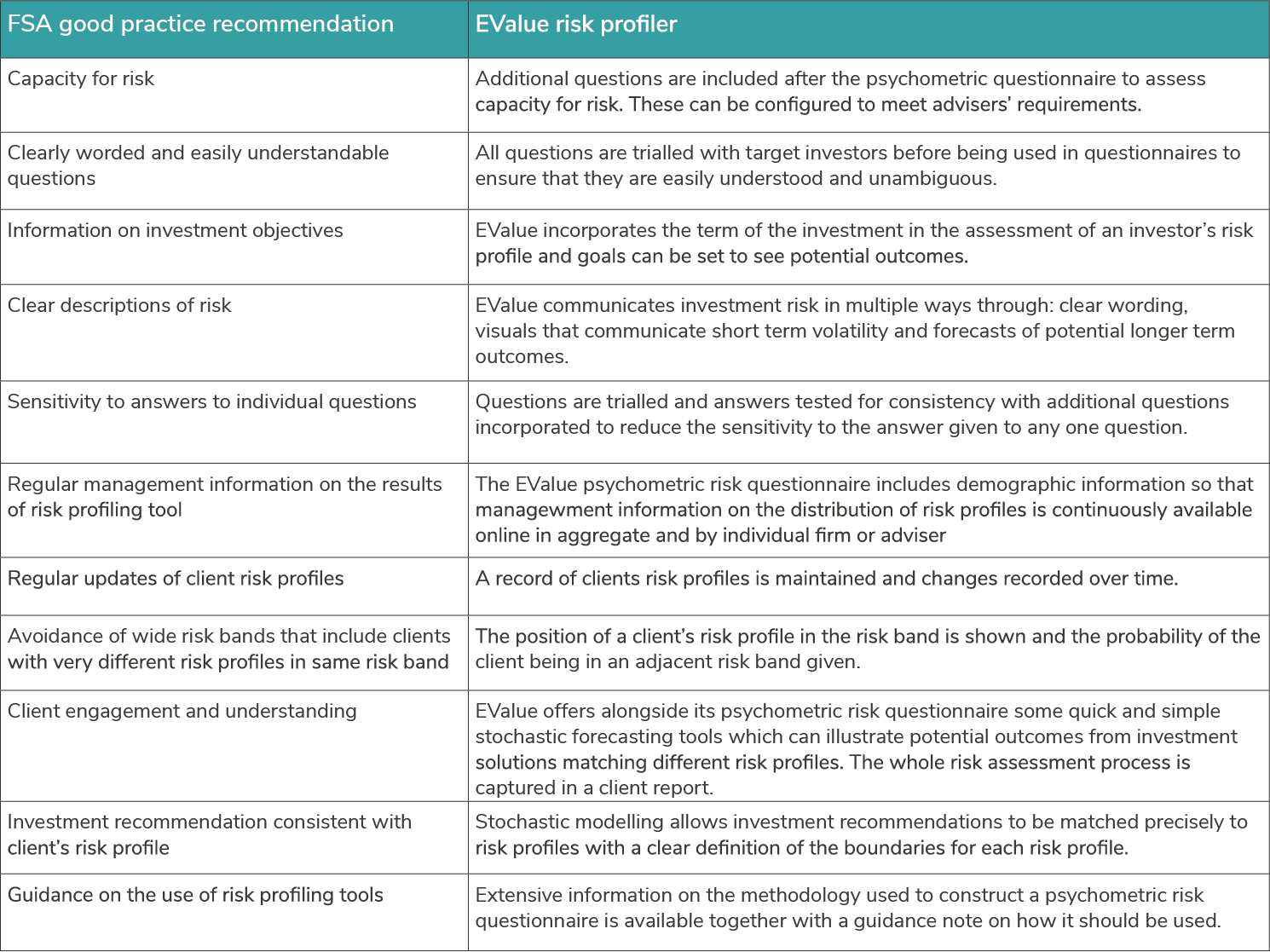

EValue offers all the best practice elements that an adviser needs to ensure that investment recommendations can be made which are suitable to a client's risk profile. These are summarised in the table below.

Yes. All risk assessments are anonymously collected along with key profiling data to ensure that the on-going reliability and quality of the questionnaire is maintained. We regularly review and update the questionnaire based on the results of the questionnaire.

The descriptors need to have the following characteristics:

- Each risk category description should be able to be understood on its own, without reference to any other risk category description. This means that words like 'more risk' or 'less risk' should not be used. Our standard risk descriptions explain the level that is expected for that risk profile without referring or comparing themselves to any other risk profile.

- Should explain the risk that is applicable to the profile and provide a means of checking that the risk level is appropriate for the investor. The wording includes a description of the type of risk that might be encountered for someone with that profile, as well as example investments for comparison.

- Be clearly differentiable between categories. To ensure a set of clearly different categories, we have produced 5 risk descriptions. When using words to describe risk it becomes difficult and rather spurious to distinguish between 10 levels of risk. The numerical and category name provides the risk level on a scale of 1 to 10 and the descriptions allow this to be communicated to the clients.

- Be consistent with the asset allocations being suggested. The EValue descriptions are designed to be used with the EValue risk questionnaire and asset allocations and as a result they are all consistent. For example, the reference to example assets within a risk category corresponds to the allocation of assets for the same risk category.

- Consider attitude to risk of investor - this is specifically what the risk questionnaire is designed to do.

- Consider capacity for loss - this should be considered in addition to the questionnaire.

- Use good quality risk questionnaire which has been validated such as that provided by EValue

- Ensure each client understands the product and investment

- Identify the client's investment objectives including the expected term and purpose of the investment

- Consider using a stochastic forecast to show what the risk means for an individual and their objectives.

- Identify clients who are not willing to take any capital risk with their money. The risk questionnaire is designed to assess the attitude to risk of individuals. An additional process will be needed to identify where there is no ability or willingness to accept any capital loss. For example, an investor may be willing to invest but not have the financial freedom to do so. You should also consider that there are other types of risk that an investor is exposed to, such as not meeting a goal which will increase with inflation, liquidity or diversification.

- Take account of the investor's investment objectives and capacity to take risk. The risk questionnaire provides the starting point for a discussion around the level of risk that an investor is prepared to accept. However, how this is implemented will vary by investment objective, time horizon and potentially also change over time. There are also other types of risk that need to be considered. We consider the stochastic forecast to be a useful method of explaining the risks to investors as it shows a personal forecast relevant to the choices and characteristics of the product and funds. It also provides figures around the level of risk that is being taken.

The following points are a guide to other tools and processes that can be provided by EV.

- Check for suitability of chosen investments compared to investor's risk profile. EV stochastic forecasting can provide a check to assess that the risk profile of the chosen funds and product are consistent with the investor's required risk profile.

- Consider relative risk of the product chosen. The EV modeller can show the risk profile of virtually all types of product, including guaranteed and structured products. This allows an easy method of showing clients the nature of risk that they will be taking.

- Illustrate the quantifiable volatility risk to clients in an engaging and personal way.

The result for the risk questionnaire provides further detail on where within each category the investor lies. The position of the triangle depends on the score that the user has achieved.

It is possible to have 'validations' on the questionnaire responses, or prompts that come up when the client has responded to questions in an apparently contradictory way. The standard questionnaires available within the free risk profiler do not include these for the following reasons:

- There is no right or wrong answer to any question, it's what the client feels about that question. Hence a client can quite appropriately have responses to questions which seem inconsistent to an adviser but are sensible to the client.

- Putting a validation on a specific question places greater emphasis on that question. However, each question in the questionnaire is given equal weight.

- It's inappropriate to validate all questions as this could lead to the client being forced to answer all questions in a similar way.

The validation of the responses to the questionnaire is more appropriately done by the adviser as part of their own sales process.

When EV's tools are implemented for an adviser group which has a defined sales process, the suite of tools can support any validation that the adviser group wishes to define. These are shown as a subtle prompt to the adviser to further pursue with their client any apparently contradictory responses. Validations can be defined between the responses to two or more questions or between the response to individual questions and the overall risk rating.

Whilst it would be possible to ask Joint Clients to sit together and complete the Risk Profiler Questionnaire, this would potentially go against expert advice that suggests a psychometric questionnaire should be completed without spending too much time considering or debating the answers. Another option would be to ask each Client to complete a Risk Questionnaire separately in relation to their joint investments and then for the Adviser to discuss the differing outcomes and liaise with both individuals to agree the appropriate risk profile for both Clients in relation to their joint investments.

Similar to assessing risk for joint Clients, when determining an appropriate level of risk to be taken by a Trust, each Trustee could be asked to complete the Questionnaire on behalf of the Trust. Results could then be compared and if the risk levels are different, the actual answers provided by each Trustee could be compared and differences discussed as a part of and during the moderation process.

This document explains how you can search for a case in the Risk Profiler tool.

This document shows how to add or amend case names in Risk Profiler.

There is an option to print a plain text list of the questions, although this is in a very basic format. The EV Risk Profiler is not designed to support an offline process, and clients should be invited to complete an online version. This can be done face-to-face with an adviser, who can log in to the service and present the questions, or by providing a link to the questionnaire via email.

You can access your account by clicking here and entering your username and password.

This can be done through the "Contact Support" button below. Once you have completed the details to confirm identity, select "Account Management" as your case type, and then "Password Reset Request". Make sure that the description contains the affected user ID which requires resetting.

This can be done through the "Contact Support" button below. Once you have completed the details to confirm identity, select "Account Management" as your case type, and then "Add Users". Enter the email address of the user(s) you would like to add to your subscription. Your billing will be updated for your next payment, to take in to account a prorated amount in addition to the monthly rate.

This can be done through the "Contact Support" button below. Once you have completed the details to confirm identity, select "Account Management" as your case type, and then "Delete Users". Enter the email address of the user(s) you would like to remove from your subscription. Please give a date when you would like the user account(s) to be disabled. If no date is given, it will be assumed that cancellation for the specified user login(s) is immediate. Your billing will be updated to reflect a prorated refund for your next month's payment. Please note, there must be at least one live user account on your subscription for the life of your account.

This can be done through the "Contact Support" button below. Once you have completed the details to confirm identity, select "Account Management" as your case type, and then "Cancel Account". Your request will be logged, and your 30 day cancellation period will begin from that day.